They have produced the documentation to the Secretary of the Cabinet of The Bahamas to be supplied to the Prime Minister and the Attorney General showing the bad practices of Colina.

The executives of those companies charge that Colina’s controlling shareholders purchased the company from its former owners with funds which were for the protection of policy holders.

In a letter to the Cabinet Secretary, they said if the various acquisitions announced by Colina are approved by regulators, “we believe that they would have a significant adverse and long-term impact on the approximately 70,000 policyholders, the minority shareholders, the staff of the relevant companies, and generally the financial services sector and the national economy.”

The executives said that it is essential for The Government to be fully informed of all relevant issues before formulating its final policy decision regarding Colina’s purchase of Imperial Life Financial and Canada Life.

The executives said that it is essential for The Government to be fully informed of all relevant issues before formulating its final policy decision regarding Colina’s purchase of Imperial Life Financial and Canada Life.

In their December 29 letter, the company executives also said that it appears that Colina and Imperial are already “actively engaged in integrating their operations.”

Two days following that letter, the Ministry of Financial Services and Investments issued a public release warning Colina “against premature action pending the lawful consideration of the regulators.”

The executives of the companies banding together to block the approval of the acquisitions are Lynda Gibson, executive vice president and general manager of Atlantis Medical Insurance Limited; Patrick Ward, president of Bahamas First Holdings Ltd; Anwar Sunderji, president and CEO of Fidelity Bank & Trust International Limited; Greg Sweeting, president of British American Insurance Company of The Bahamas Ltd.; Cedric Saunders, president of Insurance Management (Bahamas) Ltd.

These charts were taken from documents presented to the prime minister by top executives in the insurance and banking sectors.’

A. Bismark Coakley, president of Sunshine Insurance (Agents & Brokers) Ltd.; Patricia Hermanns, president of Family Guardian Insurance Co. Ltd.; Marc Shirra, general manager of Security & General Insurance Co.; Marvin Bethel, managing director of J.S. Johnson & Co. Ltd.; and Steve Watson, managing director of RoyalStar Assurance Ltd.

The Bahama Journal last week published details of the financial transactions of Colina Insurance Company. Since then, Colina has asked the Journal to apologize for the statements published which they claim are false. They are also threatening a lawsuit against this newspaper.

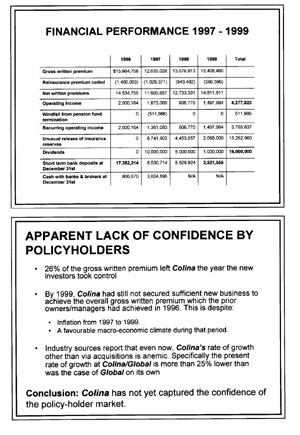

In today’s edition, the Journal publishes the financial performance record of Colina from 1997 – 1999, which can are published.ᅠ (At right.)

In the original article, we made the point that certain companies acquired by Colina were raided.

The present controlling shareholders of the company entered the market in 1997 via the purchase of Colina from Cigna.

Based on the consolidated financial statements of Colina and accompanying notes, it was shown that when Cigna owned the company, cash in the bank representing premiums was $17,353,314.

By 1999, after the current shareholders had possession for two years and 8 months, cashᅠ in the bank was $2,521,555.

The statements also show that $10 million was paid in dividends in 1997 to current shareholders.

Whereas the former owners did not declare a dividend, choosing instead to build up the company, the new owners did so every year – an aggregate of $16,000,000 – more than 4 times the aggregate of the operating income earned during the corresponding period of two years and eight months.

The operating income of Colina failed up to 1999 to sustain the level realized in 1996 by the former managers and owners of the company.

“The current management team at Colina has not yet proven its effectiveness at managing a life and health insurance company,” the executives pointed out.

Notes in the consolidated financial statements of Colina in November 1999 show that “In 1998, the Company changed its Appointed Actuary and the review of the previous reserve assumptions and methodology by the new Actuary led to an unusual release of reserves of $4,453,058.

“The unusual change in reserves was made retroactively as of 1 December, 1997 and has been reported as an unusual item in the consolidated statement of income and retained earnings for the year ended 30 November 1998.”

At the year-end prior to the new owners taking control of the company, the company only had $806,670 “Cash with Banks and Brokers”. By the end of 1997, this figure had increased to $3,004,896, inclusive of funds placed with Colina Financial Advisers, a Broker, according to documents provided by the consortium of insurance executives.

But Colina President Jimmy Campbell insisted at a press conference this week that his company stands firmly on its financial integrity and strength.

The new Colina would be by far the largest non-banking financial group.

With about 70 percent ordinary life insurance market share, it would dwarf the next largest life company by a margin of at least 5 to 1, based on premium income. It would also have leadership standing in the pension fund management sector and would be the largest health insurer.

“Domination of the ordinary life insurance industry and leadership of the pension fund management industry, represent the base for an enormous and unfettered capacity to influence much in the capital markets,” the 10 companies noted.

They continued that, “It is not in the interest of The Bahamas for there to be such a concentration of influence over the capital markets of the country at this stage in the development of those markets.”

The Bahama Journal